TL;DR

Actuarial valuation determines your employee benefits costs through key assumptions about discount rate, salary growth, and attrition patterns. You’ll learn how workforce demographics, plan types, and regulatory requirements affect your projected benefit obligation. This article explains the calculation methods actuaries use, including present value modeling and cashflow projections. Discover which factors most impact your benefit costs and how to manage them effectively for accurate financial planning.

Understanding what drives your employee benefits obligation costs isn’t just about budgeting. It’s about making informed decisions that affect your company’s financial health and employee satisfaction.

With private industry workers averaging $12.77 per hour for benefits and public sector employees reaching $23.03 per hour, the stakes are high. The actuarial valuation process determines these costs through complex calculations considering multiple variables.

Your organization’s benefit costs depend on factors ranging from workforce demographics to regulatory requirements. Getting this calculation right means the difference between accurate financial planning and unexpected budget overruns.

Factors Affecting Actuarial Valuation of Employee Benefits Costs

Multiple interconnected elements determine your final employee benefits obligation. Each factor carries significant weight in the actuarial valuation process.

Workforce Demographics

Age distribution fundamentally shapes your benefits and costs. Older employees typically require higher healthcare premiums and approach retirement benefits sooner.

Gender composition affects costs differently across benefit types. Women often utilize healthcare benefits more frequently, while men may have higher life insurance costs.

Family status creates cascading effects. Employees with dependents drive up family health coverage costs, with average annual premiums reaching $25,572 for family coverage in 2023.

Health profiles within your workforce directly impact medical benefit costs. Pre-existing conditions and chronic diseases increase premium calculations and projected benefit obligations.

Organization Size

Company size creates economies of scale opportunities. Larger organizations negotiate better rates with benefit providers due to increased bargaining power.

Small businesses face higher per-employee costs as they lack the volume discounts available to larger companies and often pay 18-20% more for comparable benefits.

Risk pooling improves with size. Larger employee groups spread risk more effectively, reducing the impact of high-cost claims on overall premiums.

Administrative costs per employee decrease as organizational size increases. Fixed costs spread across more employees create efficiencies in benefit plan management.

Geographic Location

Regional variations significantly impact benefit costs. Healthcare costs vary by up to 400% between different metropolitan areas.

Cost-of-living differences affect salary-based benefits calculations. Higher cost areas require adjusted salary growth assumptions in actuarial valuations.

State and local regulations create additional cost layers. Some regions mandate specific benefits or coverage levels not required elsewhere.

Healthcare provider networks vary regionally. Areas with limited provider options often see higher negotiated rates and reduced cost containment opportunities.

Legal and Regulatory Requirements

Compliance costs represent mandatory minimums. Legally required benefits account for approximately 25.5% of total benefit costs, according to recent data.

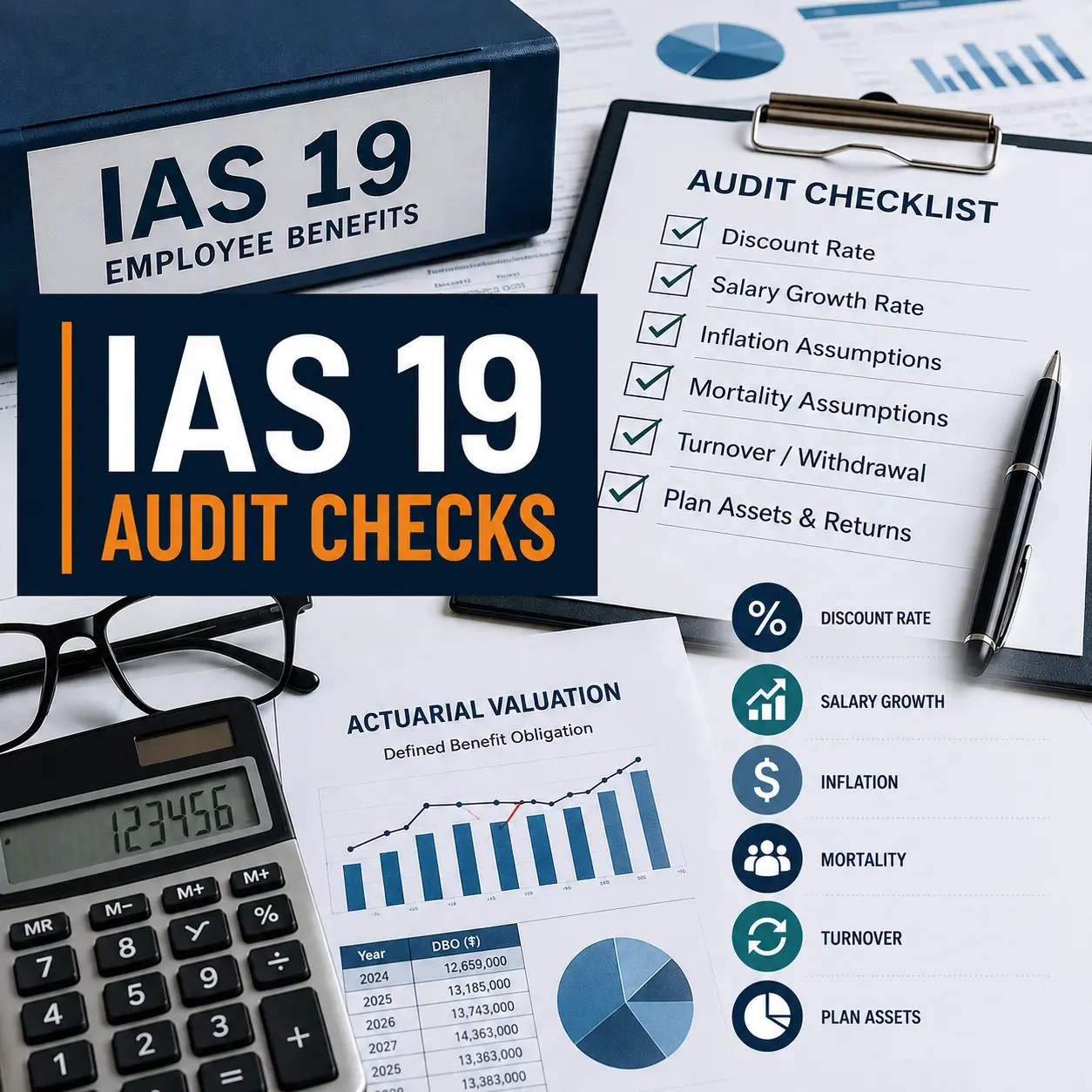

The IAS 19 requirements for international operations add complexity. These standards mandate specific actuarial valuation methodologies affecting how to calculate end-of-service benefits.

Local labor laws influence benefit structures. Different jurisdictions require varying levels of termination benefits, healthcare coverage, and retirement contributions.

Tax implications vary by location and benefit type. Understanding these differences helps optimize benefit design while maintaining compliance.

Market Competition

Competitive pressures drive benefit enhancement needs. Companies must balance cost control with talent attraction and retention requirements.

Industry benchmarks establish baseline expectations. Technology companies typically offer more generous benefits than manufacturing firms, which affects comparative costs.

Talent markets influence benefit priorities. High-demand skill areas require premium benefit packages to attract and retain employees.

Economic conditions affect competitive positioning. During talent shortages, benefit costs increase as companies compete for workers.

Employee Feedback and Preferences

Employee preferences directly impact utilization rates. Unused benefits still carry administrative costs, while heavily utilized benefits increase claims expenses.

Generational differences create varied benefit demands. Younger employees often prefer flexible benefits, while older workers prioritize traditional healthcare and retirement plans.

Communication effectiveness affects benefit value perception. Well-communicated benefits provide a better return on investment through improved employee satisfaction.

Usage patterns help predict future costs. Historical utilization data informs actuarial assumptions about employee benefit consumption trends.

Also checkout our blog: Why Employee Benefits Valuation Is More Critical Than You Think.

Types of Employee Benefits

Understanding benefit categories helps identify cost drivers and optimization opportunities. Each type carries different actuarial considerations.

Short-term Employee Benefits

Wages and salaries form the foundation of employee compensation. These direct costs average $29.86 per hour for civilian workers.

Paid leave benefits require careful accrual accounting. Vacation and sick leave accumulation create present value obligations requiring regular measurement.

Bonuses and incentive payments need actuarial consideration when they’re tied to service periods. Performance-based compensation affects projected benefit obligations.

Healthcare premiums for current coverage represent immediate costs. Single coverage averages $8,951 annually while family coverage reaches $25,572.

Post-Employment Benefit Plans

These benefits create the most complex actuarial valuation challenges. They require sophisticated modeling of future obligations and present value calculations.

Defined Contribution Plans

Employer contributions create predictable costs. Companies know their obligation upfront, typically ranging from 3-6% of employee salaries.

Investment risk transfers to employees. This shift reduces employer liability but may require higher contribution rates to remain competitive.

Administrative costs remain relatively stable. These plans require less complex actuarial valuation compared to defined benefit alternatives.

Vesting schedules affect actual costs. Employees leaving before full vesting reduce the employer’s ultimate obligation.

Defined Benefit Plans

These plans require extensive actuarial valuation using the projected unit credit method. The process considers salary growth, attrition rates, and discount rate assumptions.

Projected benefit obligations depend on multiple variables, for instance, salary growth assumptions typically range from 6-10% annually, significantly affecting present value calculations.

Investment risk remains with the employer. Market volatility directly impacts plan funding requirements and annual costs.

Longevity improvements increase costs over time. Extended life expectancies mean longer benefit payment periods and higher present value obligations.

Other Long-term Benefits

Long-service awards require actuarial assessment. These benefits often increase with tenure, creating higher obligations for stable workforces.

Sabbatical leave programs need present value calculations. Extended leave benefits must be measured and recognized over service periods.

Disability benefits involve complex probability assessments. Actuaries must consider the likelihood of disability and the expected benefit duration.

Healthcare continuation benefits extend beyond employment. These post-employment medical benefits require separate actuarial valuation.

Termination Benefits

Severance pay obligations vary significantly by jurisdiction. Some countries require substantial termination payments based on service length and salary levels.

Notice periods create immediate cost obligations. Required advance notice or payment instead of affecting cash flow planning.

Redundancy benefits may include enhanced pension benefits. These additional costs require an actuarial assessment of their present value impact.

Voluntary termination incentives need careful costing. Early retirement packages can create significant actuarial gains or losses depending on take-up rates.

Insurance

Life insurance costs depend on coverage amounts and employee demographics. Group policies provide cost advantages but still require actuarial assessment.

Disability insurance premiums reflect workforce risk profiles. Occupational hazards and employee age distribution affect premium calculations.

Professional liability coverage varies by role. Executive-level positions often require higher coverage limits affecting per-employee costs.

Travel insurance for business purposes creates variable costs. Companies with extensive travel requirements face higher per-employee expenses.

Retirement and Savings

Employer matching contributions create predictable costs when properly managed. Typical matching ranges from 25-100% of employee contributions up to certain limits.

Profit-sharing plans create variable costs tied to company performance. These arrangements require careful actuarial planning for budget predictability.

Stock option plans involve complex valuation methodologies. Fair value accounting requires sophisticated modeling of option values and vesting patterns.

Retirement planning services add administrative costs. Financial education and counseling programs improve employee satisfaction but increase per-employee expenses.

Legally Required Benefits

Social security contributions represent mandatory costs. Employer portions are typically fixed percentages of covered wages up to annual limits.

Unemployment insurance rates vary by company experience ratings. Organizations with higher turnover face increased premium costs.

Workers’ compensation premiums reflect industry risk classifications. Manufacturing and construction companies typically pay higher rates than office-based businesses.

Healthcare mandates create minimum coverage requirements. Compliance costs vary significantly by jurisdiction and required coverage levels.

Additional Compensation

Performance bonuses require accrual accounting when tied to service periods. These obligations must be measured and recognized as employees earn them.

Commission structures create variable compensation costs. Sales-based organizations face higher volatility in total compensation expenses.

Educational assistance programs provide tax advantages but create immediate costs. Tuition reimbursement benefits require careful program design to control expenses.

Flexible spending accounts reduce payroll taxes but require administrative overhead. These programs create cost savings through tax efficiency while adding complexity.

Time Off

Paid vacation accruals create balance sheet liabilities. Unused vacation time represents a present obligation requiring regular measurement.

Sick leave policies affect both direct costs and productivity. Generous sick leave may reduce overall healthcare costs through preventive care usage.

Personal days and floating holidays provide flexibility while creating predictable costs. These benefits typically have lower utilization rates than vacation time.

Parental leave benefits vary significantly by location. Some jurisdictions require extended paid leave, while others provide only unpaid options.

Calculating Employee Benefits Costs

Accurate cost calculation requires sophisticated actuarial methods. The process involves multiple steps and complex assumptions about future events.

Actuarial Valuation of Employee Benefits

The actuarial valuation process determines the present value of future benefit obligations. The purpose of an actuarial valuation is to calculate the ‘present value’ of payments that would be made to employees in the future as part of an employee benefit plan.

Actuaries use the projected unit credit method for defined benefit plans. This approach allocates benefit costs over employee service periods, creating smooth expense recognition.

Key assumptions drive valuation results. Actuaries start by making assumptions about future salary increment rates, attrition, and mortality rates. These assumptions significantly affect calculated obligations.

Discount rate selection critically impacts results. Discount Rate is one of the key actuarial assumptions used in employee benefits valuation and is based on the market yields on Government bonds as of the balance sheet date, with the term matching to expected future service of the company.

We generally assume salary growth between 6% to 10% per annum. However, for an organization that is actively expanding its recruitment policy or striving to retain talent, the escalation rate may vary significantly.

Attrition rates reflect expected employee turnover patterns. These assumptions significantly affect how to calculate end-of-service benefits and other long-term obligations.

Mortality assumptions use standard population tables adjusted for plan-specific factors. Life expectancy improvements continue to increase benefit costs over time.

Expense and Cashflow Studies

Expense recognition follows accounting standards requirements. IAS 19 mandates specific treatments for different benefit types and actuarial gains and losses.

Service cost represents current-year benefit accruals. This component reflects benefits earned by employees during the current period.

Interest cost accrues on outstanding benefit obligations. The discount rate multiplied by the opening obligation balance determines this expense component.

Expected return on plan assets reduces expense recognition. Investment performance affects actual costs, but smoothing mechanisms reduce volatility.

Cashflow projections help plan funding requirements. Understanding when benefits become payable enables better financial planning and liquidity management.

Asset and Liability Modelling

Asset-liability matching strategies minimize risk exposure. Proper portfolio construction can reduce volatility in benefit costs and funding requirements.

Duration matching aligns asset and liability sensitivities. This approach reduces the impact of interest rate changes on net benefit obligations.

Risk assessment identifies key sensitivity factors. Understanding which assumptions most affect costs enables better risk management strategies.

Scenario analysis tests assumption robustness. Multiple economic scenarios help assess potential cost ranges and funding requirements.

Stress testing evaluates extreme scenario impacts. These analyses help prepare for adverse conditions and ensure adequate financial resources.

Stochastic modeling incorporates uncertainty into projections. Monte Carlo simulations provide probability distributions of potential outcomes.

Managing Your Employee Benefits Obligations with Actuarial Valuation

In 2023, three-quarters of employers reported that their costs for providing employee benefits increased at least moderately. Understanding these cost factors enables better decision-making about benefit design and financial planning. Regular actuarial valuation helps maintain accurate financial reporting and supports strategic planning.

The complexity of employee benefit obligations requires professional expertise. 78% of employees are more likely to stay with an employer because of their benefits, making accurate costing essential for retention strategies. Working with qualified actuaries ensures compliance with accounting standards and provides valuable insights for cost management.

Your organization’s specific circumstances will determine which factors most significantly affect costs. Regular assessment and adjustment of benefit strategies help balance employee needs with financial sustainability.

Ready to optimize your employee benefits costs through professional actuarial valuation? Contact Prima Consulting today for expert guidance on managing your organization’s benefit obligations effectively.

Our experienced actuaries provide actuarial valuation services for HR & Finance Teams across Saudi Arabia, the UAE, Pakistan, Germany, and Europe achieve accurate valuations and strategic benefit planning.