TL;DR

Picking an employee benefits actuarial firm UAE businesses can trust decides how clean your IAS 19 numbers look at audit, how tight your end-of-service costs stay, and how fast year-end close moves. This guide shows how to judge a firm on IAS 19 depth, UAE gratuity law, DIFC and ADGM free-zone rules, compliance advisory, and system integration. It walks through end-of-service benefits valuation, audit readiness, typical cost and timeline, and the exact questions to ask before you sign. Get the pick right and reporting stays defensible, costs stay controlled, and your benefits strategy holds up for years.

Choosing the right partner for your employee benefits isn’t just about ticking compliance boxes.

It’s about finding a firm that understands UAE labor laws, speaks the language of international financial reporting, and can turn complex actuarial science into decisions your CFO can act on.

The stakes are high. Get it wrong, and you’re looking at audit complications, regulatory penalties, and financial misstatements that shake investor confidence.

Get it right, and you have a partner who helps you control costs, attract talent, and keep financial reporting clean.

Here’s the part most buyer guides skip. The firm you pick matters less than the specific questions you ask before you sign. Ask the wrong ones and even a big-name firm delivers a report your auditor picks apart. This guide walks you through selecting an actuarial employee benefits in UAE provider businesses can trust, and the questions that separate a strong firm from a slow one.

What Is an Employee Benefits Actuarial Firm in UAE?

An employee benefits actuarial firm in UAE is a specialist that values workplace benefits, such as end-of-service gratuity and pensions, and turns them into IAS 19 figures for your financial statements.

An employee benefits actuarial firm UAE companies work with values workplace benefits using mathematical and statistical methods.

These firms calculate the present value of future employee benefit obligations. They help companies meet financial reporting rules under standards like IAS 19, US GAAP, and local UAE regulations.

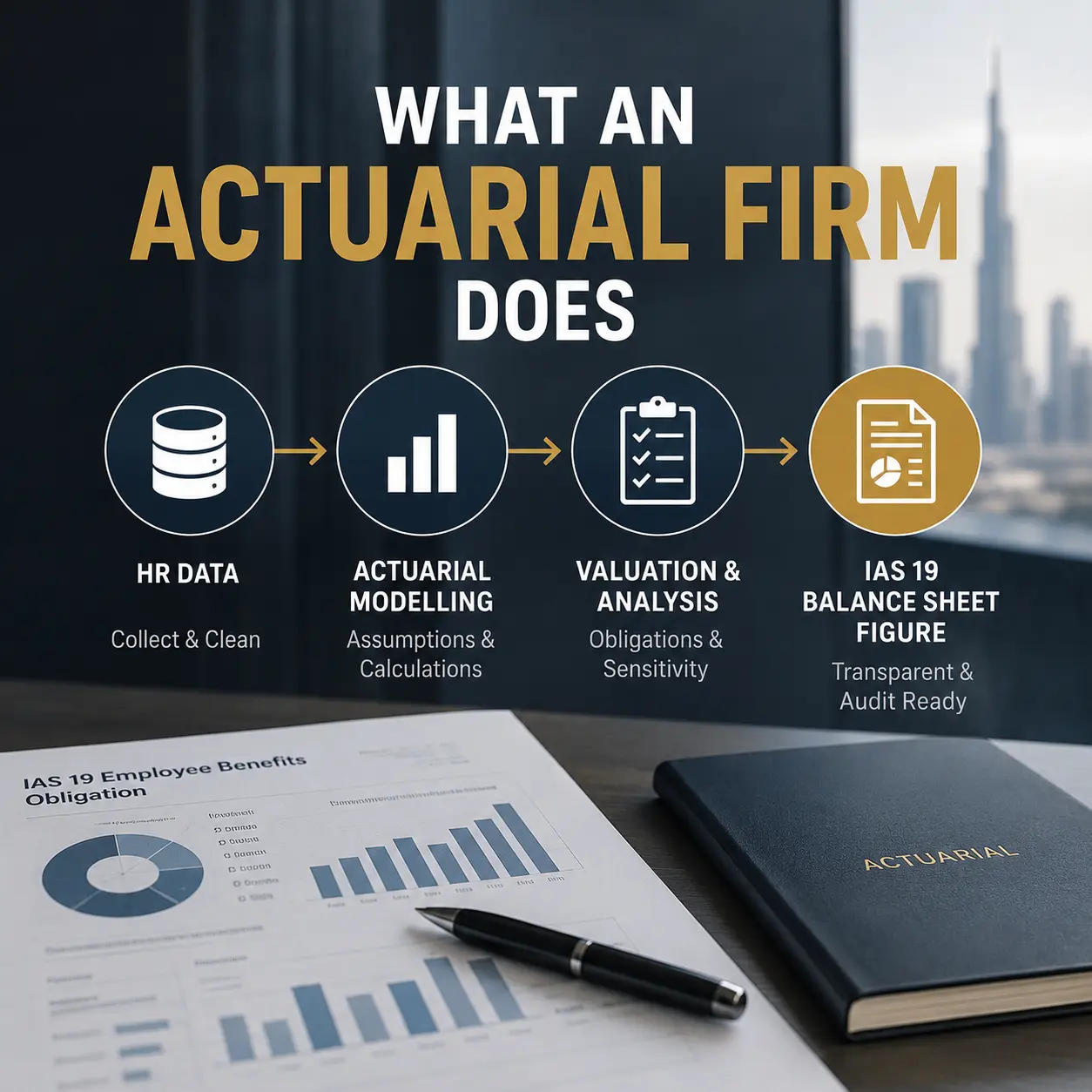

Think of them as the bridge between your HR policies and your balance sheet.

They take raw employee data, salary projections, turnover rates, and retirement patterns, then turn these inputs into precise financial figures.

Their work touches three areas that auditors care about most: financial statement accuracy, regulatory compliance, and strategic benefits planning.

In the UAE, these firms handle everything from end-of-service benefits (gratuity) to pension schemes, post-retirement medical coverage, and long-term disability plans.

Why Choosing the Right Employee Benefits Actuarial Firm Matters in UAE

Your choice of actuarial provider hits your financial health and compliance posture directly.

The wrong provider costs you in more than one way.

Financial misstatements: Inaccurate valuations lead to overstated or understated liabilities. This throws off your entire financial position.

Audit delays: Auditors read actuarial reports closely. If your provider’s work doesn’t meet audit standards, expect questions, revisions, and blown timelines.

Compliance gaps: UAE companies must follow local labor law and international accounting standards. Miss either, and you’re exposed to regulatory action.

Strategic blind spots: Good firms don’t just calculate numbers. They help you see what drives your benefit costs and how to bring them down.

The right employee benefits actuarial firm UAE companies partner with brings technical skill, local knowledge, and strategic insight to the table.

Employee Benefits Actuarial Firms in UAE: A Side-by-Side Comparison Checklist

Before you shortlist anyone, run each candidate through the same grid. Most buyers skip this and end up comparing a detailed proposal against a vague one. That’s not a fair fight, and it usually picks the better salesperson, not the better actuary.

Here’s the scorecard we’d use.

| What to check | Strong firm | Weak firm (walk away) |

|---|---|---|

| IAS 19 depth | Named qualified actuary signs the report; shows sample disclosures and sensitivity tables | Report signed by “the team”; no sensitivity analysis in the sample |

| UAE gratuity law | Models limited vs unlimited contracts, resignation bands, basic-salary-only rule | Uses one flat gratuity formula for everyone |

| Free-zone rules | Knows DIFC DEWS and ADGM treatment, asks which zone you sit in | Never mentions DIFC or ADGM |

| Audit track record | Gives audit-partner references, low revision rate, works with Big Four | Won’t share references or revision history |

| Turnaround | Commits to a dated deliverable schedule in writing | Vague on timing, “depends on our workload” |

| System integration | Pulls data from your HRIS; offers integration support and clean data templates | Emails you a spreadsheet and hopes for the best |

Score each firm across the six rows. If a candidate fails the free-zone row or the audit row, that’s usually enough to drop them, no matter how polished the pitch deck looks.

Understanding IAS 19 and Its Impact on UAE Employee Benefits Valuation

IAS 19 is the international accounting standard that governs employee benefits reporting.

It sorts benefits into four buckets: short-term benefits, post-employment benefits, other long-term benefits, and termination benefits.

For UAE companies, end-of-service benefits usually fall under post-employment benefits as a defined benefit plan.

Here’s what that means for your financials.

You must recognise the present value of your obligation on the balance sheet. Service costs hit your income statement. Actuarial gains and losses from assumption changes flow through other comprehensive income.

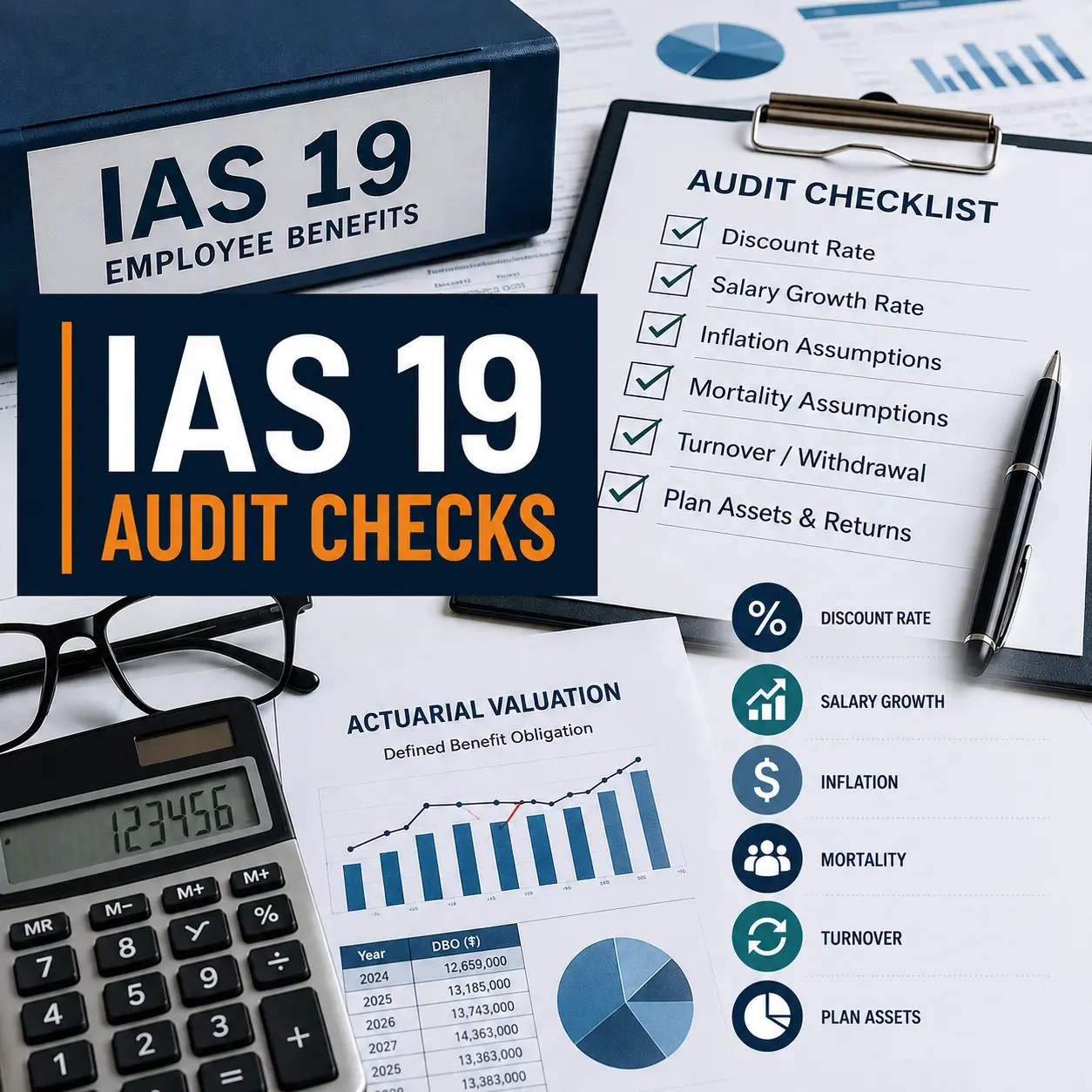

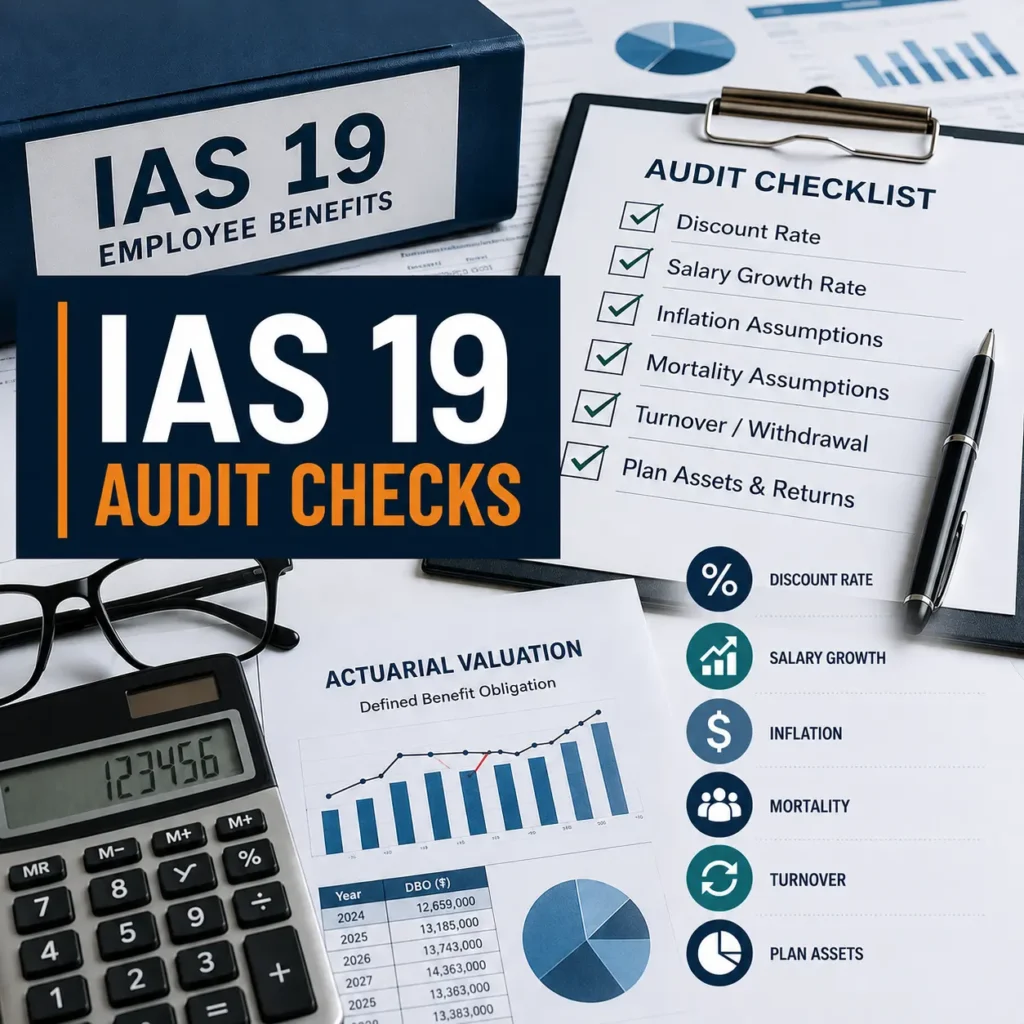

The standard asks for specific disclosures about your benefit plans, the assumptions used, and a sensitivity analysis showing how changes in key assumptions move your liability.

IAS 19 compliance isn’t optional. If you report under IFRS, your auditors will check that your actuarial valuations meet the standard.

When choosing an employee benefits actuarial firm UAE organisations trust, IAS 19 expertise is the price of entry, not a bonus.

Critical Criteria for Choosing an Actuarial Firm in the UAE

Not all actuarial firms are created equal.

Use these criteria to separate the strong contenders from the rest.

Technical Expertise in IAS 19 and International Standards

Your firm must know IAS 19 cold. Ask about their experience with IFRS reporting, US GAAP (ASC 715), and UK standards (FRS 102).

Check if they’ve worked with companies in your industry. Different sectors carry different benefit structures and reporting quirks.

Request sample reports. Good actuarial reports are clear, well-documented, and carry every required disclosure.

UAE-Specific Regional Knowledge

UAE labor law sets specific rules for gratuity calculations. Your employee benefits actuarial firm UAE partner needs to see how these interact with international accounting standards.

They should know the difference between limited and unlimited contracts. They should understand how probation periods, contract types, and resignation vs termination change gratuity.

Local economic conditions matter too. Salary growth assumptions, turnover rates, and discount rates should reflect UAE market realities, not generic regional averages.

Proven Audit Experience

Strong compliance advisory expertise is the price of entry here.

Your actuarial firm’s reports will get read hard by external auditors. The firm should have real experience with Big Four and other international audit firms.

Ask how many of their valuations have been challenged or required big revisions during audits. Good firms have low revision rates.

Request references from audit partners who have reviewed their work. That gives you unfiltered feedback on report quality.

Technology and Integration Capabilities

Modern actuarial firms run specialised software for calculations and modelling.

Ask about their tech platform. Can it handle your employee data volume? Does it plug into your HR and payroll systems?

Automated data feeds cut errors and speed up the valuation. Manual data entry raises risk and drags out turnaround.

Cloud-based platforms give you better security and access than spreadsheet-based approaches. The integration support a firm offers often predicts how painful year-end will be.

Communication and Responsiveness

Actuarial valuations aren’t set-it-and-forget-it exercises.

You need a firm that explains hard concepts in plain language. Your CFO should grasp the key drivers of your benefit costs without a math degree.

Test responsiveness during the selection itself. How fast do they reply to inquiries? Do they flag timeline and deliverables before you have to chase them?

Good firms run short teaching sessions for your finance team. They help you read assumptions, interpret results, and answer auditor questions with confidence.

Explore our advisory services

How UAE Labor Laws Affect Employee Benefit Calculations

UAE Federal Decree-Law No. 33 of 2021 governs employment relationships and end-of-service benefits.

Understanding these rules is the foundation of an accurate employee benefit valuation.

Gratuity eligibility: Employees who complete one year of continuous service qualify for end-of-service gratuity. For unlimited contracts, employees receive 21 days of basic salary for each of the first five years, and 30 days for each year after that. For limited contracts, the formula is the same, but termination before contract end changes the payout.

Resignation vs termination: If an employee resigns before five years of service, they get reduced gratuity. After five years, they get the full amount. If the employer terminates without cause, the employee receives full gratuity regardless of tenure.

Salary components: Only basic salary counts toward gratuity. Allowances, bonuses, and other pay don’t factor in.

These legal rules build the base for actuarial valuations. Your employee benefits actuarial firm UAE consultant must model resignation probabilities, termination rates, and salary progression inside this framework.

DIFC and ADGM vs Mainland: How Free-Zone Rules Change EOSB Valuation

Here’s a gap most guides ignore, and it’s the one that trips up companies with staff inside financial free zones.

Mainland UAE end-of-service benefits follow Federal Decree-Law No. 33. But DIFC and ADGM run their own employment regimes, and the valuation changes with them.

DIFC and the DEWS scheme: Since 2020, most DIFC employers moved from a lump-sum gratuity to the DIFC Employee Workplace Savings (DEWS) plan, a funded defined contribution arrangement. That shift matters for IAS 19. A funded DC scheme is accounted for very differently from an unfunded defined benefit gratuity. If your firm treats DIFC staff like mainland staff, the numbers are wrong before the modelling even starts.

ADGM: ADGM sits under its own employment regulations and permits qualifying alternative schemes too. The treatment turns on whether your arrangement is a defined benefit obligation or a funded contribution plan.

Mixed workforces: Plenty of groups run mainland entities and a DIFC or ADGM entity side by side. That means two different accounting treatments in one set of financials. Ask any candidate firm directly: how do you handle a group with mainland, DIFC, and ADGM staff in the same valuation? If they pause, keep looking.

This one question tells you more about a firm’s real UAE depth than any brochure.

Overview of Actuarial Valuation Methods for End-of-Service Benefits

UAE end-of-service benefits need the Projected Unit Credit Method under IAS 19.

Here’s how it works.

The method projects each employee’s final salary at retirement or termination. It then works out the benefit they’ll receive under UAE labor law.

That future benefit gets discounted back to present value using a discount rate based on high-quality corporate bonds.

The calculation leans on a few key assumptions:

Salary growth rate: How much will salaries rise each year?

Turnover rates: What share of employees leave each year? This shifts by age, tenure, and job category.

Discount rate: What rate should convert future payments to present value? It has to reflect the time value of money and risk-free rates.

Retirement age: When do employees typically retire or leave?

The method spreads benefit cost across each year of service. That builds a smooth expense pattern over an employee’s career.

What a UAE IAS 19 Actuarial Valuation Costs and How Long It Takes

Buyers always want this number, and most firms dodge it. So let’s be straight about the shape of it, even though every engagement prices differently.

Cost tracks three things: headcount, number of benefit plans, and how clean your data is.

A single end-of-service gratuity valuation for a small UAE company, say under 100 staff with tidy HR data, sits at the low end. A group with several thousand employees, multiple contract types, DIFC and mainland entities, and messy source data sits far higher. The driver is rarely the maths. It’s the data cleanup and the number of moving parts.

Timeline usually runs two to four weeks from clean data to signed report. The catch word is “clean.” If hire dates, basic salary splits, or contract types are missing, that clock doesn’t start. We’ve seen a two-week job stretch to six because half the salary data mixed allowances into basic pay.

One honest limit here. Anyone who quotes you a fixed fee before seeing your data is guessing. A good firm scopes first, then prices. Ask for a written scope and a dated schedule before you sign anything.

Technology and Audit Readiness in UAE Actuarial Services

Technology separates modern actuarial firms from traditional ones.

Leading firms run proprietary or commercial software that automates calculations, scenario modelling, and reporting. Purpose-built tools like the IFRS Tech IAS 19 valuation tool generate gratuity and EOSB reports against IAS 19 in minutes instead of weeks.

Data integration: The best platforms pull employee data straight from your HR systems. That kills manual data entry errors and speeds up the whole job.

Scenario modelling: What happens if you change assumptions? Good software lets you model different scenarios on the spot.

Audit trails: Every calculation should be documented and traceable. Auditors need to see how you got from raw data to the final liability figure.

Audit readiness goes past technology, though.

Your employee benefits actuarial firm UAE provider should hand over full documentation of methodology, assumptions, and calculations. Reports should include a sensitivity analysis showing how results shift when key assumptions vary.

They should answer auditor questions fast. Last-minute scrambling during audit season is a sign of poor prep.

Ask about their audit support. Do they charge extra for auditor meetings? How quickly do they respond to audit inquiries?

Common Challenges in Employee Benefit Actuarial Valuations in UAE

Even experienced companies hit snags in benefit valuations.

Data quality issues: Incomplete or wrong employee data leads to unreliable valuations. Missing hire dates, salary information, or contract types create problems.

Fix: Run regular data audits. Work with your actuarial firm to find data gaps before valuation work starts.

Assumption selection: Choosing the right discount rates, salary growth, and turnover assumptions takes judgment and local market knowledge.

Fix: Partner with firms that carry UAE-specific experience and can defend assumptions to auditors.

Contract type complexity: UAE companies often run employees on different contract types with different benefit entitlements. Modelling that accurately is hard.

Fix: Work with providers who offer strong integration support to track contract types and feed the data to actuarial models.

Timing pressures: Year-end close deadlines don’t wait for perfect data. How do you balance accuracy with speed?

Fix: Start valuation work early. Hand preliminary data to your employee benefits actuarial firm UAE team before year-end so they can catch issues in advance.

Steps to Evaluate and Compare UAE Actuarial Service Providers

Follow this structured run when working through the questions to ask a benefits consulting firm.

Step 1: Define your requirements. List all benefit plans needing valuation. Note any special reporting needs or tight deadlines.

Step 2: Research potential firms. Look for firms with UAE presence and employee benefits expertise. Build a shortlist of three to five candidates.

Step 3: Request proposals. Send detailed RFPs asking about methodology, experience, technology, pricing, and timeline.

Step 4: Assess technical capabilities. Review sample reports. Check whether they meet IAS 19 disclosure rules and explain things clearly. This is a key factor in selecting a UAE pension consultant.

Step 5: Check references. Contact current clients. Ask about work quality, communication, and how they solve problems when things go wrong.

Step 6: Assess cultural fit. You’ll work with this firm for years. Do they get your business? Can they explain hard topics simply?

Step 7: Compare value, not just price. Look at total cost of ownership across service packages, including add-ons for audit support and consulting.

Step 8: Set clear governance. Define roles, deliverables, timelines, and communication from day one.

The Role of Local Expertise and Regional Compliance in Firm Selection

Local knowledge isn’t a nice-to-have. It decides whether your valuation holds up and your audit runs smooth.

Regulatory updates: UAE labor law changes often. Your employee benefits actuarial firm UAE partner should track legislative changes and adjust valuations. Recent updates to Federal Decree-Law No. 33 changed calculation methods for certain contract types. Firms without local presence missed these.

Market data: Salary growth assumptions, turnover rates, and economic projections must reflect UAE conditions, not regional averages. A firm using Gulf-wide assumptions might overstate or understate your liabilities against one using UAE-specific data.

Audit firm relationships: UAE-based actuarial firms know the local audit partners and what they want to see. That speeds up the audit.

Cultural understanding: Employment practices in the UAE differ from other markets. Probation periods and notice requirements shape turnover and termination assumptions. An expert team with deep UAE experience bakes these into their models.

How Actuarial Firms Support Long-Term Employee Benefits Strategy

Smart companies use their employee benefits actuarial firm UAE partnership for more than annual compliance.

Benefits plan design: Before you launch a new benefit, model its long-term cost. Actuaries can project five to ten year liabilities under different design options. Review benefits plan design case studies to see what worked elsewhere.

Cost control: Which benefits drive the most cost? Where can you adjust eligibility or formulas to hold expenses down without hurting staff satisfaction?

Scenario planning: What if you grow headcount by 30%? What if salary growth speeds up? Model these to see the financial hit before it lands.

M&A due diligence: Buying a company? Value their benefit obligations as part of deal pricing. Spot any unfunded liabilities or compliance issues early.

Financial forecasting: Fold benefit cost projections into your annual budgets and long-range plans using proven actuarial employee benefits optimization in UAE techniques.

The best partnerships go past compliance. They help you make smarter calls about your total rewards programs with ongoing support.

Who Prima works with

Across industries and geographies, delivering measurable outcomes

🏦

Banks & Financial Institutions

IFRS 9 ECL models, credit risk, impairment methodology, regulatory reporting

🛡️

Insurance & Takaful Companies

IFRS 17 implementation, actuarial modelling, GMM/VFA/PAA, CSM calculations

🏢

Corporates & Multinationals

End-of-service gratuity, IAS 19 valuations, IFRS 15/16, internal controls

📈

Investment & Asset Managers

IFRS 9 classification, fair value (IFRS 13), derivative valuations, hedge accounting

🏗️

Real Estate & Construction

IFRS 16 lease accounting, IFRS 15 revenue recognition, project-based reporting

🏛️

Family Offices & Holding Groups

Governance frameworks, board advisory, risk management, portfolio evaluation

Trusted by Leading Organizations

Over 100 organizations across the Middle East, Europe and Asia trust Prima Consulting.

Frequently Asked Questions About UAE Employee Benefits Actuarial Firms

Partnering with the Right Employee Benefits Actuarial Firm in UAE

Choosing an employee benefits actuarial firm UAE organisations can rely on comes down to technical skill, local expertise, and strategic fit.

The right partner brings more than compliance. They give you the insight to control costs, shape benefits, and make informed calls about total rewards.

Focus on firms with proven IAS 19 depth, real UAE market knowledge, and strong audit track records. Push for clear communication and modern technology that plugs into your systems. And ask the free-zone question early, because it filters out the pretenders fast.

Don’t rush this. Check references, review sample work, and test cultural fit before you sign.

Want a partner who reads both the numbers and your business? Prima Consulting handles actuarial & employee benefits solutions in UAE, pairing technical depth with practical judgment. Our enterprise risk management and risk advisory services sit alongside the actuarial work. Talk to us about your employee benefits strategy and reporting needs.

Free Consultation

Ready to discuss your IAS 19 valuation?

Prima’s actuaries value end-of-service benefits for mainland, DIFC, and ADGM employers across the UAE. First conversation is always free, no pitch, just expertise.