TL;DR

IAS 36 advisory services help your organization prove that asset values on the balance sheet are defensible, not just compliant. This guide covers how impairment testing works, when reviews are required, how to measure recoverable amount, and what auditors look for. You’ll also learn how to identify CGUs correctly, handle goodwill impairment, and coordinate IAS 36 IFRS compliance services alongside IAS 19 valuations. Impairment of assets accounted for 12% of UK FRC review cases in 2023/24, making this a high-stakes area. Read the full guide to decide when to bring in asset impairment specialists.

IAS 36 Advisory Services for Impairment Compliance

Impairment testing is one of those areas where the gap between “we followed the standard” and “we did it right” can be surprisingly wide. IAS 36 advisory services exist to close that gap. Whether you’re preparing for a year-end audit or reassessing assets after a tough market cycle, the standard demands more than a checkbox exercise. It asks for documented judgment, defendable assumptions, and a process that holds up under scrutiny.

Demand for IAS 36 advisory services has grown steadily as global economic volatility and rising interest rates have placed more assets at risk of impairment.

According to the UK Financial Reporting Council, impairment of assets accounted for 12% of all cases opened in corporate reporting reviews during 2023/24. That’s not a small figure. It signals that impairment remains a persistent weak spot for many organizations, large and small. If your team is navigating this terrain without specialist support, the risk of getting it wrong is real.

This guide walks you through everything you need to know, including where IAS 36 impairment consultants add the most value.

What Is Asset Impairment Under IAS 36?

Asset impairment occurs when an asset’s carrying amount exceeds its recoverable amount. The carrying amount is what appears on the balance sheet, i.e., cost less accumulated depreciation and any previous impairment losses.

The recoverable amount is the higher of two figures: fair value less costs of disposal (FVLCD) or value in use (VIU). When carrying amount sits above that recoverable figure, the difference must be recognized as an impairment loss immediately.

IAS 36 applies to a broad range of assets. These include property, plant and equipment, intangible assets, goodwill, right-of-use assets, and investments in subsidiaries. It does not apply to inventories, deferred tax assets, or financial assets covered by IFRS 9.

For a foundational overview of how this standard works, see the IAS 36 Impairment Basics guide.

When Is an Impairment Review Required?

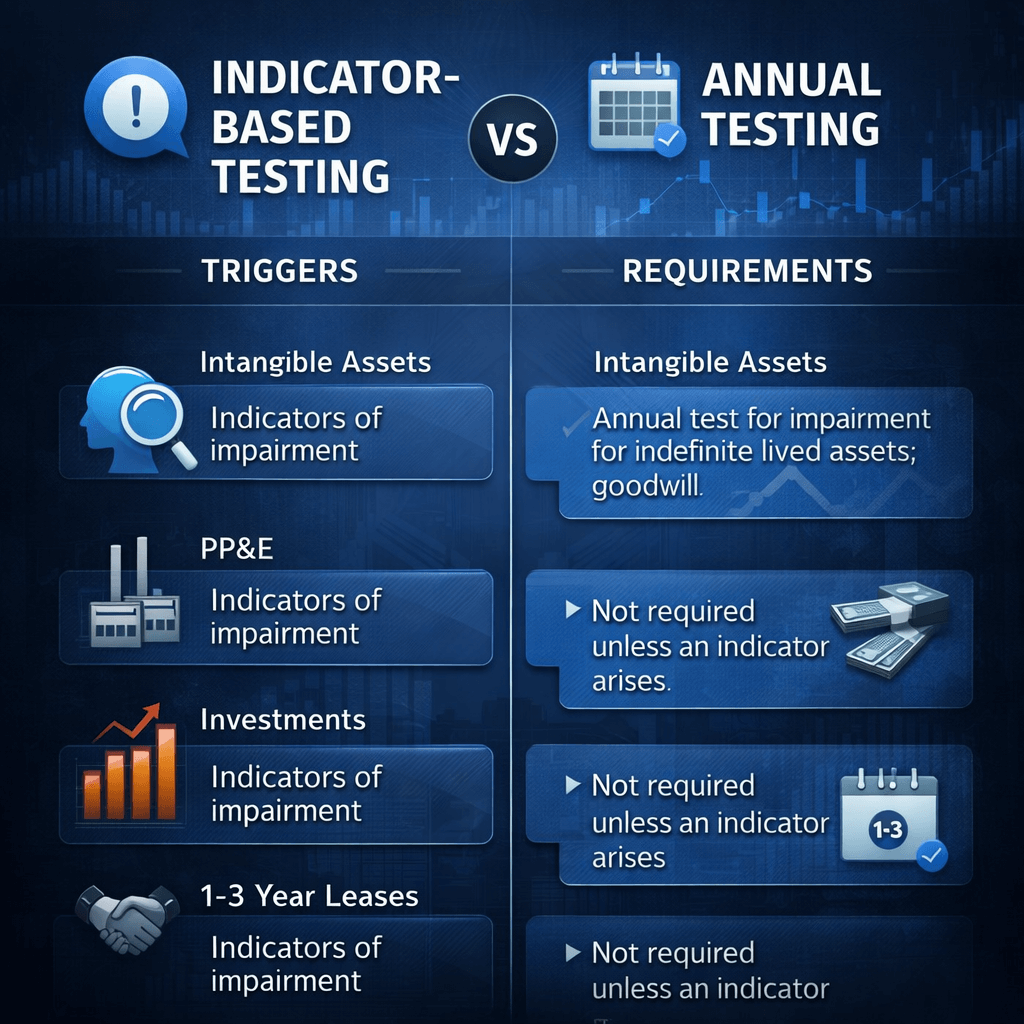

The standard sets out two distinct triggers for impairment reviews.

For most assets, a review is only required when there are indicators of impairment present at the reporting date. That said, there’s an important exception. Goodwill, intangible assets with indefinite useful lives, and intangible assets not yet available for use must be tested annually, regardless of whether any indicators exist.

That annual test for goodwill can be performed at any point during the year, as long as it’s done at the same time each year. Different assets within the same entity can be tested at different dates, which gives management some flexibility in scheduling.

Indicator-Based vs. Annual Impairment Testing

The distinction matters for how you resource and plan your reviews. Indicator-based testing means you’re watching for signals and acting when they appear. Annual testing is a fixed obligation, non-negotiable for certain asset classes.

External indicators worth monitoring include market value declines, adverse changes in the business environment, significant rises in interest rates, and situations where market capitalization falls below the net carrying amount of assets. Internal indicators include obsolescence, physical damage, changes in how an asset is used, and underperformance against forecasts.

Here’s a practical point: identifying an indicator doesn’t automatically mean a write-down follows. It means a quantified test is required. That test may well confirm that no loss exists. The indicator just opens the door to the process.

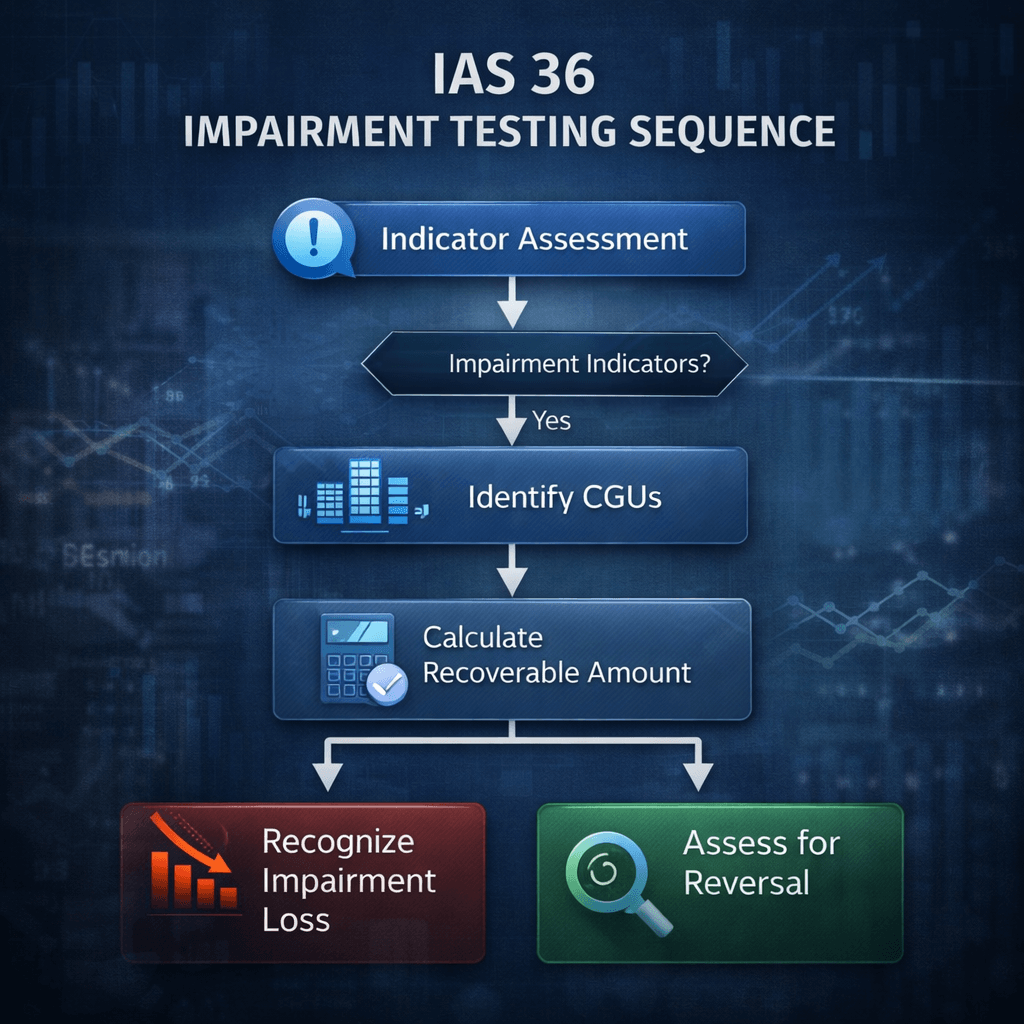

How the Impairment Testing Process Works

Identifying Impairment Triggers

Start by looking at the asset or group of assets in question. At each reporting date, management must assess whether any indicators of impairment are present, drawing on both internal and external sources of information.

You might be wondering: what counts as a meaningful trigger? A sustained drop in a commodity price that directly affects an asset’s earning capacity, a change in technology that reduces an asset’s useful life, or a reorganization that alters how an asset generates cash can all qualify. Economic conditions post-2022, including interest rate increases and inflationary pressures, have pushed many entities to reassess assumptions they’d previously treated as stable.

Because of that shift in the macro environment, many finance teams found their prior discount rate assumptions no longer reflected current conditions, prompting impairment charges that hadn’t been anticipated in earlier budgets.

Measuring Recoverable Amount

Once a test is required, the next step is estimating recoverable amount. You calculate both FVLCD and VIU, then use whichever is higher. If either measure already exceeds the carrying amount, there’s no need to calculate the other.

FVLCD reflects what a market participant would pay for the asset, minus disposal costs. It draws on market-based evidence, where available, or income approaches applied with market participant assumptions.

VIU, on the other hand, is entity-specific. It’s based on management’s own projections of future cash flows, discounted back to present value using a pre-tax rate. IAS 36 requires that those projections cover a maximum of five years (aligned to approved budgets), with a terminal growth rate that’s steady or declining and doesn’t exceed the long-run average growth rate for the relevant market.

The discount rate used in VIU calculations is a particularly sensitive judgment area. It should reflect the time value of money and the risks specific to the asset, and it’s typically derived from a weighted average cost of capital (WACC) before adjusting for tax. Getting this number right, and being able to justify it, is one of the most common areas where IAS 36 impairment consultants provide direct value.

To understand the full testing methodology, the IAS 36 impairment testing resource covers the process in detail.

Recognizing and Recording Impairment Losses

Once you’ve confirmed that carrying amount exceeds recoverable amount, the impairment loss equals the difference between the two. It goes through the income statement immediately, unless the asset is carried at a revalued amount under another standard, in which case the loss may first offset any revaluation surplus.

After recognition, the asset’s new carrying amount becomes its new depreciation base. Future depreciation charges are recalculated on that new base. This isn’t optional or deferred, the re-basing happens in the same period as the recognition.

It’s worth noting: impairment is a one-way street for most assets. You can’t simply write an asset back up because market conditions improve. Reversals are permitted under IAS 36 for most assets, but only when the specific circumstances that caused the original impairment have changed. Goodwill is the exception; once written down, it stays written down.

Goodwill and Complex Asset Impairment

How Goodwill Impairment Differs

Goodwill doesn’t generate cash flows independently. It benefits from the broader business it’s attached to. That’s why IAS 36 requires goodwill to be allocated to cash-generating units (CGUs) or groups of CGUs that are expected to benefit from the synergies of the acquisition.

The annual impairment test for goodwill is applied at the CGU level, comparing the CGU’s carrying amount (including the allocated goodwill) against its recoverable amount. If the CGU fails the test, goodwill is written down first, then other assets are reduced on a pro-rata basis.

Cash-Generating Unit Considerations

A CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of those from other assets. Identifying your CGUs correctly is foundational. Errors here can distort the test results significantly.

Key factors in CGU identification include how management monitors operations, how products or services generate independent cash flows, and whether assets could be sold separately. In a retail context, for example, each store might be a separate CGU. For a manufacturing group, a production line might qualify.

Once established, CGU boundaries shouldn’t change without reason. Arbitrary changes to avoid recognizing losses are a known area of regulatory scrutiny.

Reversal of Impairment Losses

If the conditions that caused an original impairment no longer exist, IAS 36 permits a reversal. The reversal amount is capped at what the asset’s carrying amount would have been, had no impairment been recognized in prior periods (after adjusting for depreciation).

In practice, reversals occur most often where specific circumstances have clearly changed. A manufacturing entity, for instance, might reverse an impairment on equipment if a market that had closed down reopens and demand recovers. That said, reversals require the same rigor of documentation as the original loss. You need to show that the change in recoverable amount is linked to a verifiable change in circumstances, not just an improvement in market sentiment.

Documentation and Audit Expectations

Required Evidence for Impairment Testing

Auditors want to see a clear, documented process, not a spreadsheet with a conclusion. The evidence file should include the basis for CGU identification and boundaries, the cash flow projections used in VIU calculations with their source (approved budgets, board papers), the methodology and inputs for the discount rate, any sensitivity analysis performed, and the rationale for key assumptions like growth rates and margin profiles.

Documentation should also explain why any assumptions differ from prior periods, particularly if economic conditions have shifted. If you’re using a market approach for FVLCD, you’ll need to show the comparable transactions or multiples applied and why they’re appropriate.

Auditor Focus Areas and Common Gaps

Regulators have been clear about their concerns. In 2023/24, four UK companies restated parent company financial statements for impairment of investments in subsidiaries, reflecting the ongoing challenge of getting this right.

Auditor attention tends to concentrate on three areas. First, the reasonableness of cash flow projections, particularly when they show improving trends that aren’t supported by current trading. Second, the discount rate, specifically whether it reflects current market conditions and asset-specific risk. Third, the identification of CGUs and whether their boundaries are consistent with how management actually runs the business.

Common gaps include using budgets that were approved before a material change in trading conditions, applying post-tax rates without correctly deriving the pre-tax equivalent, and failing to document the sensitivity of conclusions to changes in key assumptions.

Economic Factors Affecting Impairment Reviews

Market Volatility and Asset Valuation

Market volatility directly affects both the FVLCD and VIU calculations. That’s where IAS 36 advisory services tied to current market data become particularly valuable. Rising discount rates, which followed central bank rate increases from 2022 onward, compress present values significantly. An asset that looked recoverable at a 7% discount rate may show impairment at 10%.

At the same time, market-based evidence for FVLCD can become unreliable during periods of low transaction volumes. If comparable deals aren’t happening, observable data is thin, and the reliance on income approaches increases. That places greater weight on management judgment and, by extension, greater auditor scrutiny.

Forecast Assumptions and Sensitivity Analysis

The forecast period matters enormously. IAS 36 caps VIU projections at five years for the detailed period, with a terminal value beyond that. The growth rates applied to that terminal value should not exceed the long-run average rate for the market or industry.

Sensitivity analysis isn’t technically required by IAS 36, but it’s strongly encouraged by auditors and regulators, particularly for goodwill-carrying CGUs. Showing how the conclusion changes if the discount rate moves by 1% or if revenue growth falls by 2% gives reviewers confidence that management understands its own assumptions and their limits.

If a CGU passes impairment testing only by a small margin, that margin should be explicitly disclosed. Users of financial statements need to know when a CGU is sensitive to reasonably possible changes in assumptions.

Choosing Expert Impairment Advisory Support

Qualifications to Look for in Advisors

Not all IAS 36 advisory services are built equally. When evaluating IAS 36 advisory services, look for a combination of technical accounting knowledge and practical valuation experience. The advisor should know IFRS deeply and be able to translate that knowledge into defensible models.

Beyond credentials, ask about their experience with your industry sector. Impairment assumptions for a retail chain differ from those for an extractive industry asset or a software business. Discount rates, growth assumptions, and CGU structures all vary significantly. An advisor who’s worked across sectors can spot assumptions that look unusual in context.

You’ll also want experience working with auditors. The best IAS 36 impairment consultants know what auditors look for and can help you build a file that stands up to that scrutiny without unnecessary rework.

When to Seek External Impairment Expertise

There are moments when internal capacity, no matter how strong, isn’t enough. Acquisitions that require goodwill allocation to new CGUs, first-time IFRS adoption, restructuring exercises that change how assets generate cash flows, or significant changes in the macro environment are all natural points to bring in external asset impairment specialists.

Regulatory reviews or audit disputes are another clear trigger. If your auditor is pushing back on assumptions and you’re struggling to build a case, that’s not the moment to go it alone.

Impairment advisory pricing varies depending on scope, asset complexity, and geographic footprint. That said, the cost of expert support is almost always lower than the cost of a restatement, a qualified audit opinion, or regulatory action. For a full overview of how specialist support works in practice, visit the IAS 36: Impairment of Assets service page.

IAS 19 Valuation vs. IAS 36 Impairment

Key Differences in Objectives and Methods

IAS 19 and IAS 36 often come up together in the context of financial reporting compliance, but they serve very different purposes. IAS 19 deals with employee benefits, primarily defined benefit pension obligations. Its focus is on actuarial assumptions: discount rates for pension liabilities, mortality rates, salary growth projections. The valuation produces a liability figure on the balance sheet.

IAS 36, by contrast, focuses on the asset side. It asks whether an asset is worth what it’s carried at, using either market or income-based evidence. The two standards use different discount rate frameworks, different projection horizons, and different risk-adjustment approaches.

What they share is the need for specialist input. Both require informed judgment, documented assumptions, and defensible outputs.

Coordinating Financial Reporting Compliance

For many entities, IAS 36 and IAS 19 work falls in the same reporting cycle. A pension actuarial review coincides with year-end impairment testing. That’s actually an opportunity. Discount rate assumptions, macro-economic projections, and long-run growth expectations can often be shared and cross-checked between the two workstreams.

Coordinating IAS 36 IFRS compliance services with your IAS 19 valuation work can reduce duplication, improve consistency, and make the overall audit process smoother. Asset valuation consultants who work across both areas are better placed to support that coordination.

Frequently Asked Impairment Questions

How Often Should Impairment Testing Occur?

Goodwill, indefinite-life intangibles, and intangibles not yet in use must be tested annually, regardless of indicators. For all other assets, testing is triggered by the presence of impairment indicators at the reporting date, based on IAS36 audit support standards. Annual tests can be conducted at any point in the year, as long as the timing is consistent from year to year.

Can Impaired Assets Recover Value?

Yes, for most assets. IAS36 allows reversals of impairment losses when the circumstances that caused the original loss have demonstrably changed. The reversal is capped at the amount that would have been the carrying amount had no impairment been recognized.

The key exception is goodwill. Once impaired, goodwill cannot be reversed under IAS 36, regardless of subsequent performance.

What Happens After an Impairment Loss?

After an impairment loss is recognized, the asset’s recoverable amount becomes its new carrying amount. Depreciation is recalculated based on that lower figure over the asset’s remaining useful life. The impairment loss itself is recorded on the income statement in the period it’s identified, with disclosure requirements covering the amount, the segment or CGU affected, and the event or circumstance that led to the loss.

Getting IAS 36 Right: Why Expert IAS 36 Advisory Services Matter

Strong IAS 36 advisory services aren’t just a regulatory formality. They’re a practical safeguard against errors that show up in audit findings, restatements, and in some cases, enforcement action. The complexity of VIU modeling, CGU identification, goodwill allocation, and discount rate derivation means that even experienced finance teams benefit from specialist input at key moments.

If your organization is facing a year-end impairment review, a significant restructuring, or regulatory pressure on prior period disclosures, the right IAS 36 advisory services can make the difference between a clean opinion and a qualified one. Talk to the team at Prima Consulting to find out how they can support your IFRS compliance across impairment testing, recoverable amount estimation, and audit readiness.